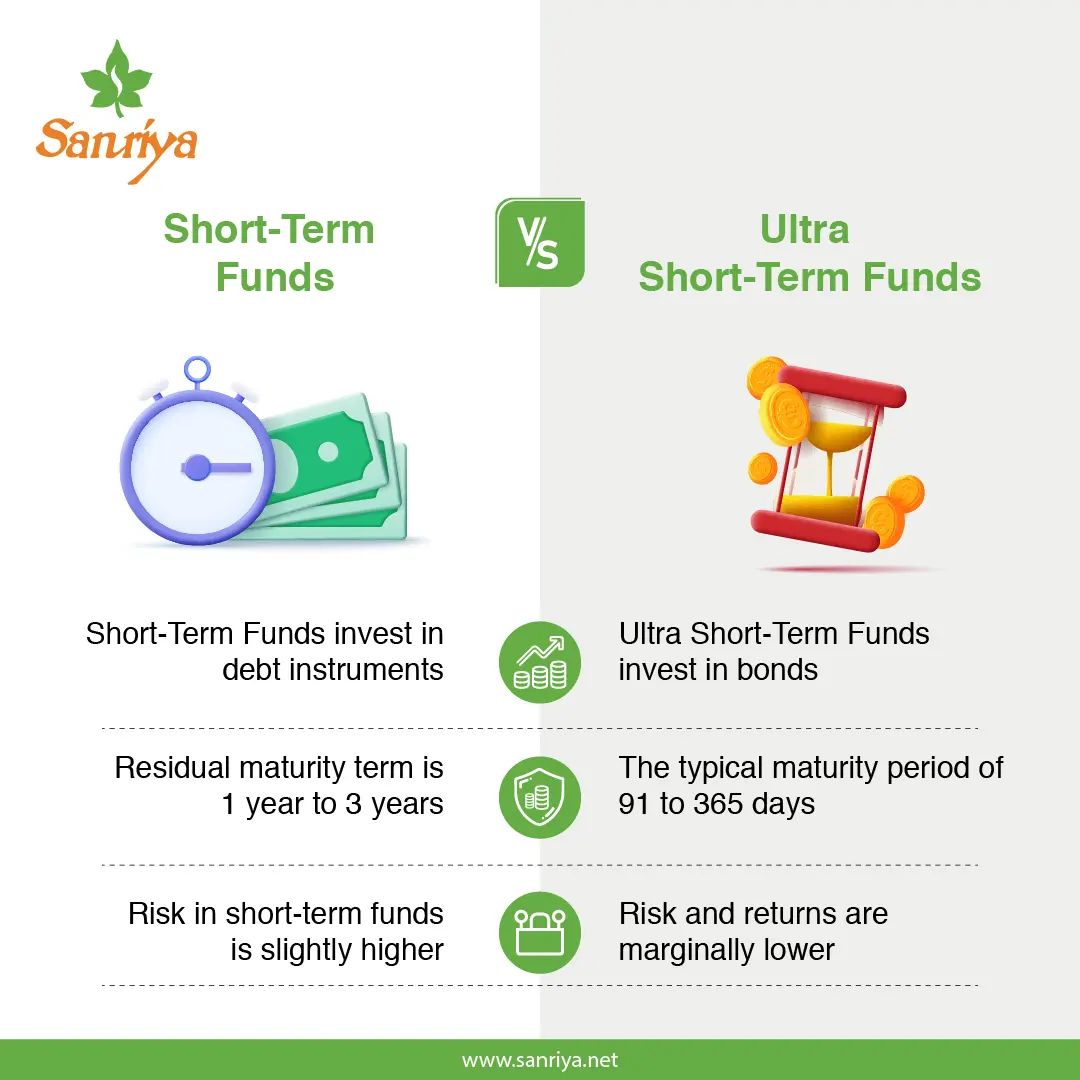

Short-term funds primarily invest in debt securities with maturities ranging from one to three years. These funds aim to provide a slightly higher return than traditional savings accounts or fixed deposits while maintaining a relatively low level of risk. They are suitable for investors looking for a balance between safety and returns, making them a popular choice for short-term financial goals or emergency funds.

Ultra short-term funds, on the other hand, focus on even shorter-term debt instruments with maturities of less than one year. These funds are designed for investors seeking higher liquidity and very low risk. They provide a safe parking place for surplus cash, often offering slightly better returns than fixed deposits. Ultra short-term funds are suitable for those who may need to access their money at short notice.

Both types of funds offer benefits such as professional management, diversification, and the potential for better returns compared to traditional savings options. They are also more tax-efficient than fixed deposits, with potential tax benefits for long-term investors. Additionally, they provide the convenience of easy entry and exit, making them suitable for those who need flexibility in their investments.

Investors should choose between short-term and ultra short-term funds based on their specific financial goals and risk tolerance. It’s essential to consider factors like investment horizon and the current interest rate environment when making a decision.

In conclusion, short-term and ultra short-term funds are valuable options for individuals looking to earn a reasonable return on their surplus cash without taking on excessive risk. These funds offer flexibility, safety, and the potential for better returns, making them popular choices for managing short-term and emergency funds.